.png)

Risk Signal Desensitisation

- Martin Davies

- Apr 26, 2024

- 1 min read

Updated: May 5, 2024

There are different levels of maturity in Risk Management Analysis and in Causal Capital, we’re finding many of the more advanced risk management teams we’re working with are starting to consider complicated secondary Risk Assessment / Modelling techniques. Don’t get me wrong, risk reporting (matrix inclusion / exclusion discussions aside), risk registration, control assessment are all important agendas to be entertained but they are in the getting it together end of risk management.

Extending beyond these Risk Management Foundations, there is an emerging interest in reporting secondary aspects of risk management including some of the following: Strategic & Business Model Risk and Business Model Concentration. Today we’re going to look at the serious but underestimated impacts of Creeping Normality or Risk Signal Desensitisation on Risk Assessment models.

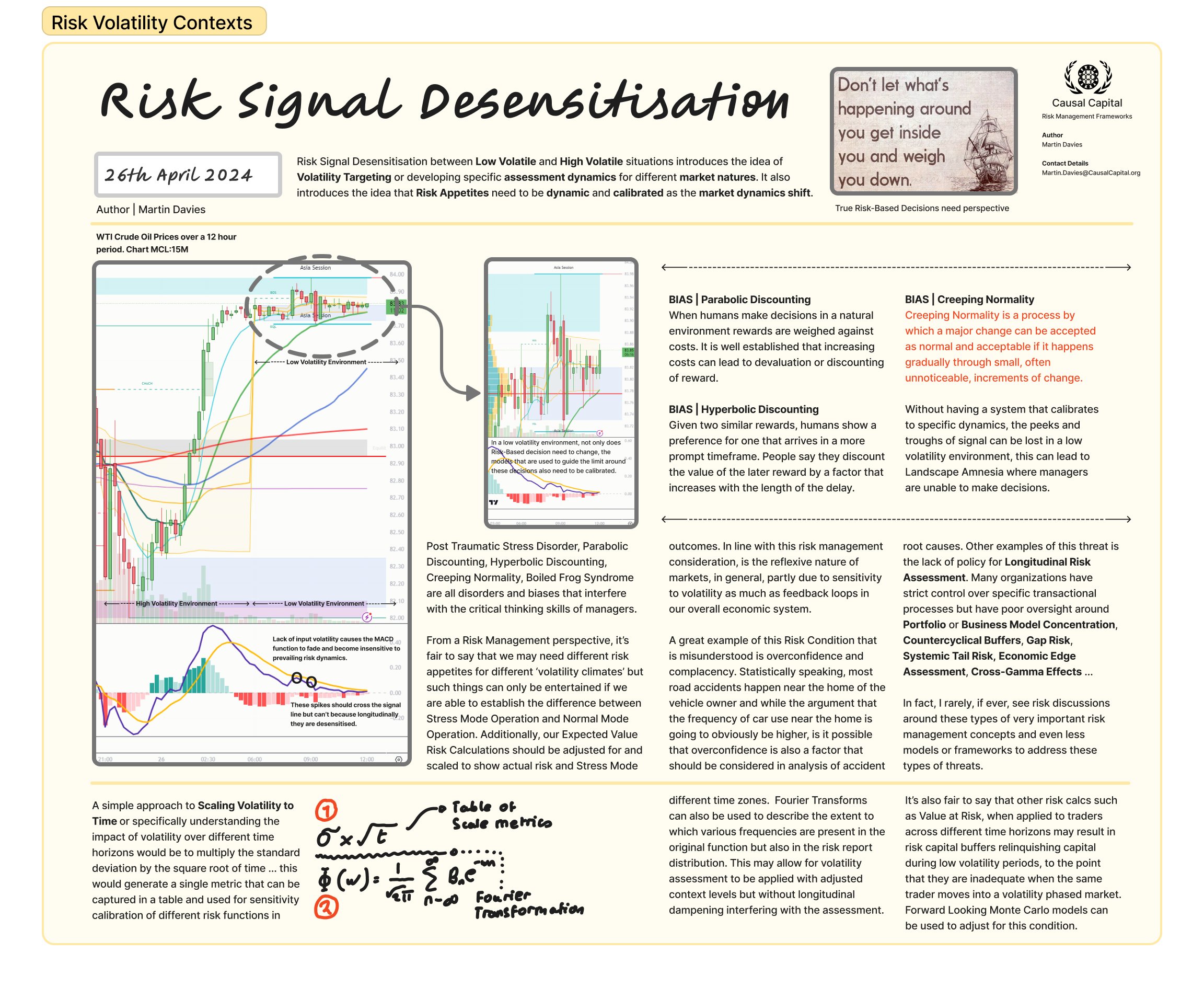

Risk Signal Desensitisation | Martin Davies (Click Image to enlarge)

To date, I have not seen that many Volatility Scaled Risk Assessments beyond the Countercyclical Buffer Reports that form part of the Basel III Regulatory Risk Reporting agenda. Stress Testing Risk Reports do kind of touch on this space and articles like Volatility Targeting [LINK] are very much part of what we're talking about in our white paper above.

It is based on adjusting the level of exposure of the entire portfolio to target a constant level of volatility

Volatility Targeting | Quantpedia

Basically, this is an explorative Risk Modelling idea that we're putting forward that simply put, focusses on the differing risk attitudes & appetites around Normal Mode vs Stress Mode Risk-Based Decision Making.

Comments